Most of us work hard at building up assets / wealth during our lifetime.

But how well do we protect them?

Generational wealth / assets / estate that get handed down attract attention, especially from the government/ tax authorities.

Inheritance tax is one such penalty/ charge placed on the ‘estate’ that we leave behind for posterity. Choosing to use a trust to pass on our assets can offer us significant peace of mind, protect our assets as well as reduce the Inheritance Tax bill.

If we gave away/ gifted all of the estate in our lifetime there would be no residual estate, and hence no IHT liability on death.

However that may not be ideal as:

- We do not know how long we will live or how much estate we would need to get to the very end.

- We may still need to be use these assets and also may not have enough decided the beneficiaries upfront or who gets what.

- The receiving parties / family members may as they may not even be mature enough to look after sudden wealth and may end up squandering it.

TRUSTS are a valuable tool in for protecting and passing wealth to future generations in a tax efficient way. Let’s take a closer look.

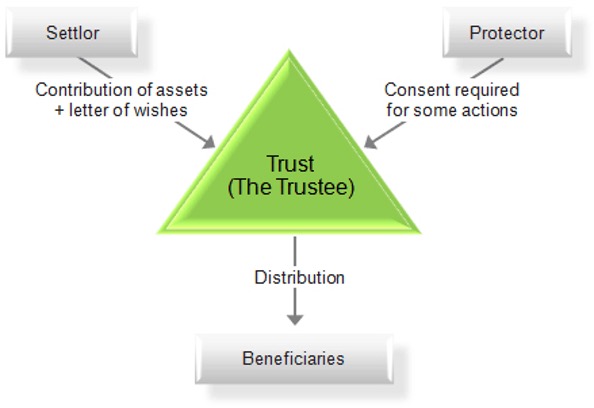

A trust as an arrangement that allocates assets into an account for the benefit of another person at a future date. For instance, we may want to leave a property to our child. However, we want them to have it when they are old enough to fly the nest and live on their own.

How to make use of TRUSTS for Inheritance tax purposes

Simply put, a trust is a legal method of protecting and managing our assets for the beneficiaries. A trust avoids handing over valuable property, cash or investment while the beneficiaries are relatively young, immature or vulnerable.

The cash / investments / property / other assets put into trust, they no longer belong to us. They now belong to the trust and sit outside our estate and that when we die their value normally won’t be counted towards the Inheritance Tax bill.

There are lots of reasons why individuals do not want to pass on their wealth directly to their beneficiaries.

- Having a Trust bypasses the time-consuming process of probate and allows the assets to be managed without waiting for a Grant from the Courts.

- A Trust can protect our share of assets for the children in the event that our partner should marry or co-habit after we are gone.

- We can place our assets in a Trust to make sure the beneficiaries receive assets in way and at a time that’s right for us and for them. Or maybe we would like the gift to be enjoyed by a group of people, such as grandchildren, whenever born.

- We have complete control and can decide on the trustees and what they can and cannot do. This may also be beneficial if we are unable to manage our financial and legal affairs due to incapacity.

- We may have concerns about irresponsible habits / behaviour patterns, level of maturity of adult children which makes them prone to poor decisions.

- Or, we may be concerned over our kids divorce and we want to protect our hard earned cash being counted as an asset.

Types of Trust

Different types of trust structures are available in the UK. A Trust allows us to retain various degrees of control over the amount and timing of extending the benefits; as well as help us extend/ restrict the list of beneficiaries.

Absolute Trust or Bare Trust

This is an arrangement whereby a settlor gives trustees cash or other assets to look after for a named beneficiary (or beneficiaries). The beneficiaries cannot be changed. Settlors must therefore be certain of who they wish to benefit from the outset.

Absolute trusts are normally used for minor children due to the fact that on reaching age 18 (16 if written under Scot’s law) the beneficiary is entitled to the trust fund.

Gifts into absolute trusts are treated as potentially exempt transfers (PET). This does not result in an immediate IHT charge, and will not be liable to IHT at all if the settlor (or donor) survives the gift by seven years. In case the settlor does die within seven years, the gift becomes a chargeable transfer which may result in an IHT liability.

Discretionary Trust

Under a Discretionary trust there are normally no named beneficiaries but instead a class of prospective beneficiaries. This class normally includes children, grandchildren and so on. Discretionary trusts offer flexibility for the trustees and can provide for several generations.

Interest in Possession Trusts

Also known as life interest trusts, these tools allow the income of the trust, after expenses, to be paid out to a nominated beneficiary or beneficiaries. They’re often used to provide for a spouse for the rest of their lifetime, with assets then passing to children after the spouse’s death.

Packaged Trust Solutions

Many trust solutions come as packaged solutions. These include gift trusts, loan trusts and discounted gift trusts which may use investment bonds as the underlying investment.

A Discounted Gift Trust is an estate planning vehicle designed for people who have excess capital that they are prepared to give away but would still like to take payments from their capital to supplement their income. The gift into trust will provide an immediate IHT saving if a discount is agreed. The whole value of the gift will be free from IHT if the settlor survives it by 7 years. Unless an absolute trust is being used, any gifts above their available nil rate result in an immediate charge to IHT.

In case of a Loan trust, the settlor lends money to the trust. The trustees then invest this money, typically into an investment bond, for the benefit of the trust beneficiaries.

The settlor can demand repayment of the outstanding loan at any time. If regular loan repayments are needed, the trustees can repay the loan by using the 5% tax deferred withdrawal facility from the bond. Any growth in the fund must be used for the benefit of the trust beneficiaries.

© Anu Maakan April 2024